What is a Good Company from Calculating Economic Profit?

Judging whether a company is good or not purely from its profitability could be disguising. Like everything in this world, even growth and profit have costs, and that's the cost of invested capital.

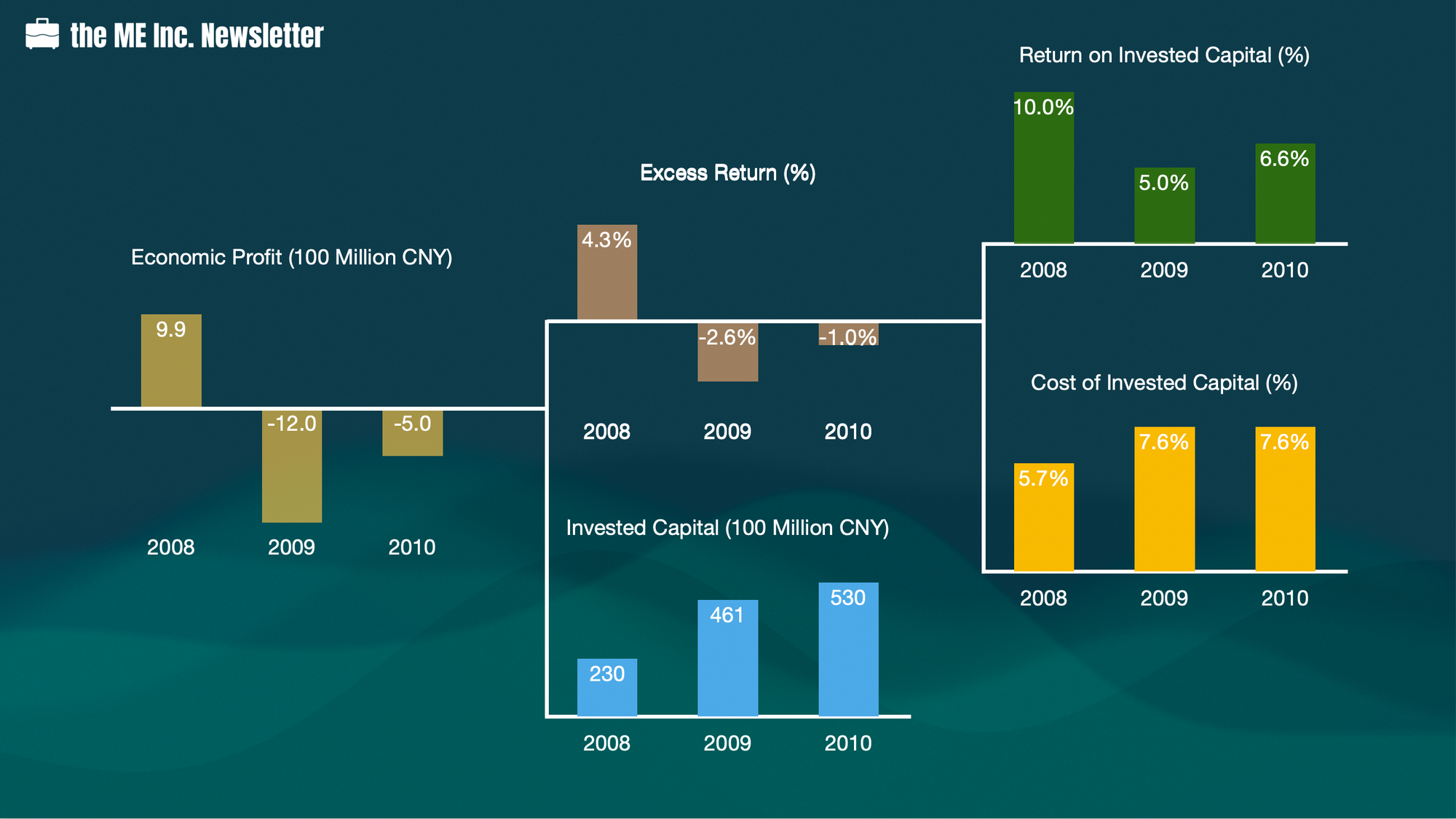

We've covered how to calculate return on invested capital in our previous episode. The rates of return on invested capital of this company in 2008, 2009, and 2010 were 10%, 5%, and 6.6% respectively. Given such figures, do you think the company is making money? To be more specific, do you think such a rate of return on invested capital is acceptable?

What we often hear is that the return on invested capital should at least be on par with loan interest rates, inflation rates, expected return of investors, or industry standards.

However, all of the above rates can be very much different from each other. Loan interests might be much lower than the average profitability rate in the industry; inflation rates could be quite different the expected return of investors. Is there any fixed benchmark for the rate of return on invested capital?

Let’s analyze this question.

At the end of the day, what the return on invested capital measures is still a type of return on investment. From the simplest sense, what any investor wants is at least not to lose money, i.e. the return should be higher than the cost. Therefore, one type of benchmark for evaluation is the cost of investment from investors. In other words, it is the cost of invested capital.

Let's assume we have calculated the cost of invested capital (we will get to the calculation of this number in the next episode) for the company in each year from 2008 to 2010, which are 5.7%, 7.6%, and 7.6% respectively.

Now that we have both the return on the invested capital and cost of invested capital, we can simply let the former minus the latter and see if the result is positve or negative. The result is often referred to as excess return. If the excess return is positive, we'd say such investment is acceptable, and if it is negative, we'd say it is unacceptable.

From our calculations, we can see that only 2008 yielded a positive excess return. Both year 2009 and 2010 yielded negative excess returns. And since we already know the invested capital for each of the three years, we can get each year's economic profit by multiplying excess return and invested capital for that particular year.

Apparently, the economic profit was only positive for the first year and negative for the rest two years. In other words, the return on investment of the company is only acceptable in 2008, not in 2009 and 2010.

This conclusion might come as extremely shocking to a lot of folks, including me. After all, the company has made billions of net profit each year at an annual average growth rate of 26%. How could a profitable and growing company be a bad investment?

The answer lies in cost; like anything in this world, growth and profitability also have prices. And if their prices (or costs) exceed the value of the growth and profitability, the investor could be better off putting her money somewhere else.

Next, we will cover how to calculate the cost of invested capital.